Want to know more?

The continued rise in investment products presented as sustainable has created the urgency to protect the market from the risk of greenwashing. According to the 2020 Global Sustainable Investment Review, Environmental Social and Governance (ESG) assets in Europe, United States, Canada, Japan and Australasia accounted for around 38% of total managed assets in these regions, with Canada recording the highest proportion of ESG assets at 62%.

Publications from the Canadian Securities Administrators (CSA) provide descriptions of what greenwashing means:

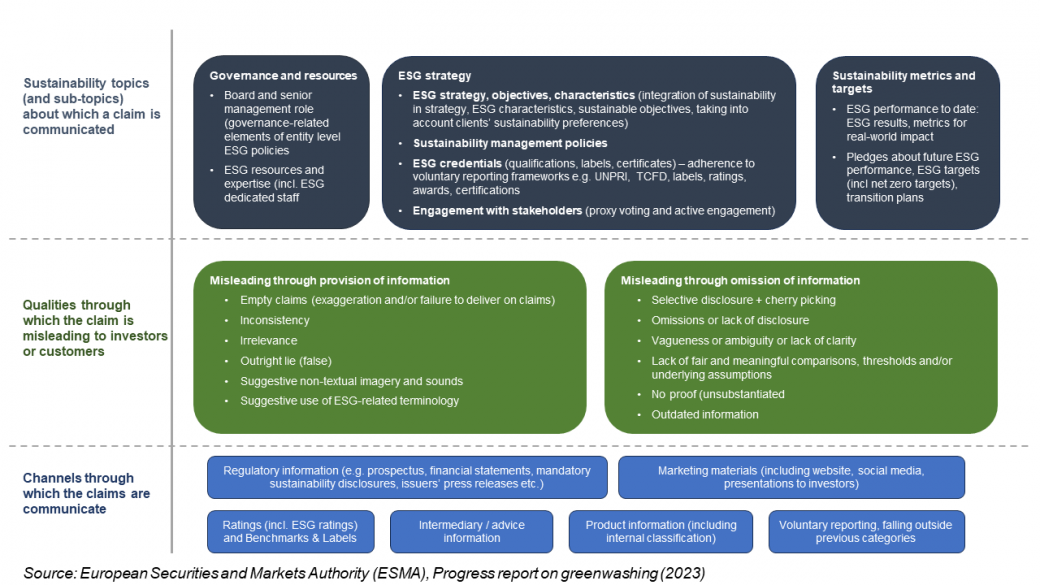

The below summarises how greenwashing can manifest in the sustainable investment value chain.

When greenwashing occurs, it can heighten traditional risks (such as credit, operational and liquidity risks) and destabilise the financial markets (by way of large-scale selloffs for instance). To this effect, securities regulators around the world are looking to clamp down on greenwashing incidents and Canada is no exception.

Below summarises key measures Canada has taken and how these compare with corresponding measures in the United States (US), which is a key economic partner for Canada and the European Union (EU), which can represent a “model” given the region’s more advanced regulatory framework around sustainable finance.

A taxonomy provides investors and companies with a common definition of economic activities that can be considered as sustainable or have a path to reach acceptable sustainability performance levels. In May 2021, the Sustainable Finance Action Council (SFAC) was launched to make recommendations to the Canadian government on critical infrastructure to attract and scale sustainable finance in Canada, one of which being an environmental taxonomy.

In March 2023, the SFAC published its report which set out recommendations for defining and implementing a taxonomy. From their report, the taxonomy would not only indicate the criteria for what qualifies as green but will also include the criteria for a transition financial instrument. The latter reflects the vital role transition finance will play for Canada to achieve its net zero ambition given the current economic dependence on fossil fuels.

The approach of setting a definition for green and transition financial activities aligns with the EU’s approach to its Taxonomy which came into force in July 2020. The EU Taxonomy set criteria for what qualifies as

The SFAC expects to publish by mid-2023 a short form taxonomy covering priority sectors and activities. A detailed taxonomy should be released by end of 2025. The SFAC’s taxonomy needs to be reviewed and approved by the Canadian Government. However, the SFAC’s version will provide a good indication of what the final taxonomy should be and Asset Managers (AMs) can use this to undertake preliminary assessments of the classification of their investment products.

The CSA released staff notice 81-334 ‘ESG-related investment fund disclosure’ to provide guidance on disclosure practices of investment funds as they relate to ESG considerations. This is to ensure marketing communications are not misleading and are consistent with funds’ offering documents. The staff notice was not intended to create a new requirement but to clarify how existing securities regulatory requirements apply to ESG-related investments.

Unlike Canada’s approach of not having additional specific requirements around ESG-related disclosures, the EU and US have imposed or intend to impose such requirements. The EU introduced the Sustainable Finance Disclosure Regulation (SFDR) which requires disclosures on how sustainability risks can affect the value and return on investments as well as the adverse impacts the investments can have on environmental and social factors. This regulation applies to financial market participants and advisors based in the EU as well as those outside the EU who market or intend to market their products to clients in the EU. In the US, the Securities and Exchange Commission (SEC) proposed rules to enhance disclosures of how certain investment advisers and investment companies, based within and outside the US, incorporate ESG into their investment practices. Final rules are expected in 2023.

The CSA’s staff notice 81-334 includes guidance on the naming of ESG investment funds. It requires there to be a clear link between funds’ names and investment objective.

The European Securities and Markets Authority (ESMA) have been more prescriptive in their consultation on guidelines for funds’ names using ESG or sustainability related terms. Part of their proposals include adopting quantitative thresholds for using ESG or sustainability related terminology in funds' names such as at least 80% of the funds’ investment holdings should meet environmental and social characteristics. Final guidelines are expected by Q2/Q3 2023.

In November 2022, the CSA issued staff notice 51-364 which set out key findings and outcome from reviewing Continuous Disclosure (CD) documents provided by reporting issuers during the fiscal year ended 31 March 2021 and 2022. They observed greenwashing issues in CD documents and voluntary documents, such as ESG reports and public surveys, and stated their expectations of how these issues should be mitigated.

The EU and US regulators have taken stricter actions upon identified incidents of greenwashing. The SEC fined BNY Mellon Investment Adviser and Goldman Sachs Asset Management for failures to consistently follow the internal ESG policies and practices they stated they had. There have been instances in different EU countries (e.g. Denmark, Germany and France) where local regulators are investigating alleged claims of greenwashing by AMs or have mandated AMs to take remedial actions where disclosures were deemed non-compliant to the SFDR rules.

As part of its 2023/2024 priorities, the CSA intends to complete a focused review of how ESG disclosures by investment funds comply with its staff notice 81-334. It will publish its findings and any updates to the guidance by December 2023. There is currently no explicit indication of enforcement actions CSA could take against specific issuers where deficiencies are identified following their reviews. Nevertheless, AMs should be reviewing the extent to which they can demonstrate adherence to 81-334 requirements to mitigate against potential litigation or legal risks arising from deemed non-compliance.

While Canada continues to strengthen the regulatory framework and clarify expectations around greenwashing, the direction of travel is clear. Therefore, Canadian AMs should be taking appropriate actions to effectively respond to future regulatory changes in Canada and international developments around greenwashing. Actions AMs can take include:

Subscribe now to our mailing list to receive our publications, articles, invitations to our events, and more.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.